House of Representatives Office of Payroll and Benefits

Executive Summary

Just a portion of Social Security benefits is subject to Minnesota income taxes. The exclusion from tax is the issue of 2 separate policies—the federal exclusion from gross income for a portion of Social Security benefits, and the Minnesota Social Security Subtraction.

Overall, approximately 33 per centum of Social Security benefits paid to Minnesota residents are bailiwick to taxation, merely approximately 62 percent of resident returns with Social Security benefits paid tax on that income. After bookkeeping for residents who do not file state revenue enhancement returns, about 45 percent of Minnesota households receiving Social Security benefits pay tax on their benefits.

This webpage describes how the federal exclusion and country subtraction are calculated, shows the income levels at which taxpayers are subject to taxes on Social Security benefits, and provides a survey of the tax treatment of Social Security in other states. It additionally includes cursory historical context on the federal exclusion and land subtraction.

Exemption from Minnesota Income Tax

A taxpayer'south Social Security benefits are fully or partially exempt from Minnesota's income tax. There are two separate tax policies that result in Social Security benefits beingness nontaxable—an exclusion in federal police that "flows through" to the taxpayer's Minnesota income tax, and an additional Minnesota-specific subtraction available for a portion of the income that is taxable federally.

The extent to which Social Security benefits are subject area to Minnesota income tax depends on the measure used. At that place are at least 3 ways to measure the extent of Social Security taxation in the state:

- The percentage of taxation returns with Social Security benefits that paid at least some tax on thei benefits.

- The percentage of resident beneficiaries that paid at least some tax on their benefits.

- The per centum of resident Social Security benefits that are subject field to tax in Minnesota.

Returns and Beneficiaries Paying Minnesota Tax on Social Security Benefits

| Full resident returns | Resident returns filed with Social Security income | Estimated total households that include a Social Security casherii | Resident returns that paid state tax on Social Security income |

|---|---|---|---|

| 2,658,000 | 565,000 | 784,000 | 352,000 |

Share of returns paying any Minnesota income taxes on Social Security benefits:

| |||

Among taxpayers filing returns, near 352,000 resident returns paid at least some Minnesota tax on their Social Security benefits in taxation twelvemonth 2017. That represents virtually 62 per centum of all resident returns filed in Minnesota with Social Security benefits.

However, research past the Social Security Trustees suggests that merely over half of Social Security recipients pay federal income tax on their Social Security benefits, and but about 72 percent of beneficiary families file income tax returns.three If the federal guess of 72 percent of beneficiaries' families filing returns applies to land returns also, then about 784,000 total households included a Social Security beneficiary,4 and about 45 percent of Minnesota families that included a Social Security beneficiary paid land income tax on their benefit.5

Social Security Benefits Subject to Minnesota Income Tax

The most contempo year for which data is available is revenue enhancement year 2022 (returns filed in 2018). In tax year 2017, virtually 565,000 resident returns in Minnesota reported about $12.8 billion in Social Security benefits. Of that amount, 48.9 percent was taxable federally, and about 41.3 per centum was taxable in Minnesota. These numbers do not account for the expansion of the Minnesota Social Security Subtraction, which was enacted in the 2022 omnibus tax bill.half dozen

The Social Security Assistants reported that about $15.968 billion in Old-Age, Survivors, and Inability Insurance (OASDI) benefits were paid to Minnesotans in 2017.seven This implies that virtually $3.1 billion in benefits were paid to taxpayers who did not file a return, likely considering they had no Minnesota income tax liability. Including residents who did non file a return, about 33 per centum of all benefits paid to Minnesota residents were subject to Minnesota income tax.

The lowest-income taxpayers pay very little taxation on their Social Security benefits, due largely to the federal exclusion. About 92 percent of the Social Security benefits subject area to Minnesota income tax is earned by taxpayers with at least $50,000 of federal adjusted gross income (FAGI), and about 72 percent is from taxpayers with at least $75,000 of FAGI.

| Federal Adapted Gross Income | Social Security benefits (millions) | Federal exclusion (millions) | Minnesota subtraction (millions) | % of benefits taxable federally | % of benefits taxable, Minnesota | Share of total taxable benefits |

|---|---|---|---|---|---|---|

| Less than $25,000 | $3,604 | $iii,521 | $69 | 0.5% | 0.four% | 0.3% |

| $25,000 to $l,000 | 2,408 | ane,638 | 362 | 32.0 | 16.9 | 7.7 |

| $fifty,000 to $75,000 | 2,076 | 653 | 337 | 68.half dozen | 52.3 | 20.5 |

| $75,000 to $100,000 | one,679 | 283 | 178 | 83.2 | 72.six | 23.0 |

| $100,000 to $150,000 | 1,823 | 280 | 17 | 84.7 | 83.7 | 28.8 |

| $150,000 and Greater | 1,234 | 185 | 0 | 85.0 | 85.0 | 19.eight |

| Total | $12,824 | $6,560 | $963 | 48.ix% | 41.iii% | 100.0% |

| Tax Year 2022 Estimates using the Firm Income Tax Simulation model. Compiled by House Enquiry. | ||||||

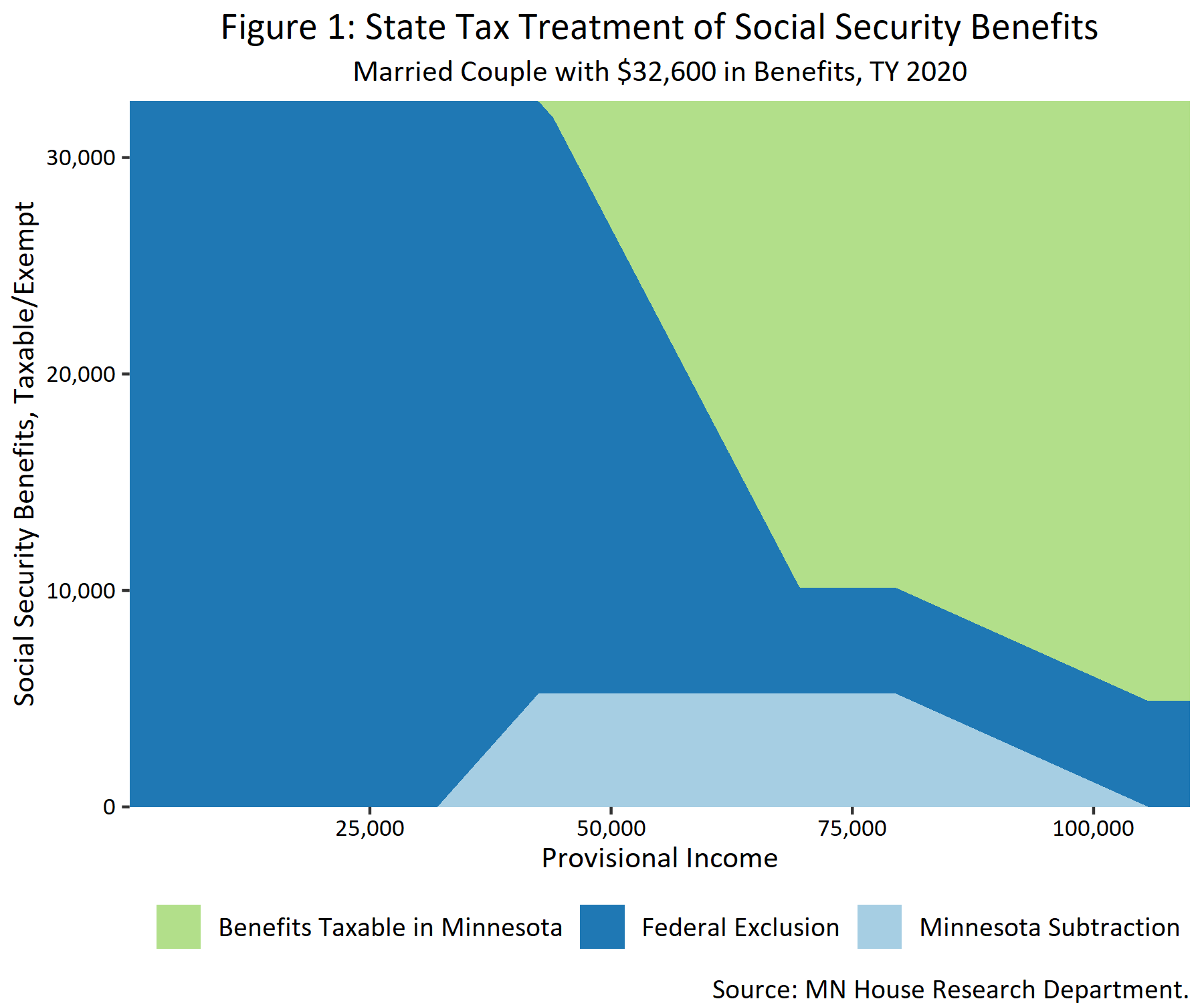

Effigy i below shows the state revenue enhancement on Social Security income in revenue enhancement twelvemonth 2022 relative to provisional income. 8 The figure shows the federal exclusion and country subtraction for a married taxpayer filing a articulation return with $32,600 in Social Security benefits, which is about twice the average annual benefit amount for a married couple receiving benefits in Minnesota.ix Taxpayers with $32,600 in Social Security benefits would likely have at to the lowest degree $16,300 in provisional income, because provisional income includes 50 percent of Social Security benefits.ten The federal exclusion is significantly larger than the country subtraction. Married taxpayers filing joint returns that receive $32,600 in Social Security benefits do non pay Minnesota tax on their income until provisional income reaches about $42,500, or when non-Social Security income plus all Social Security benefits equals $58,800.

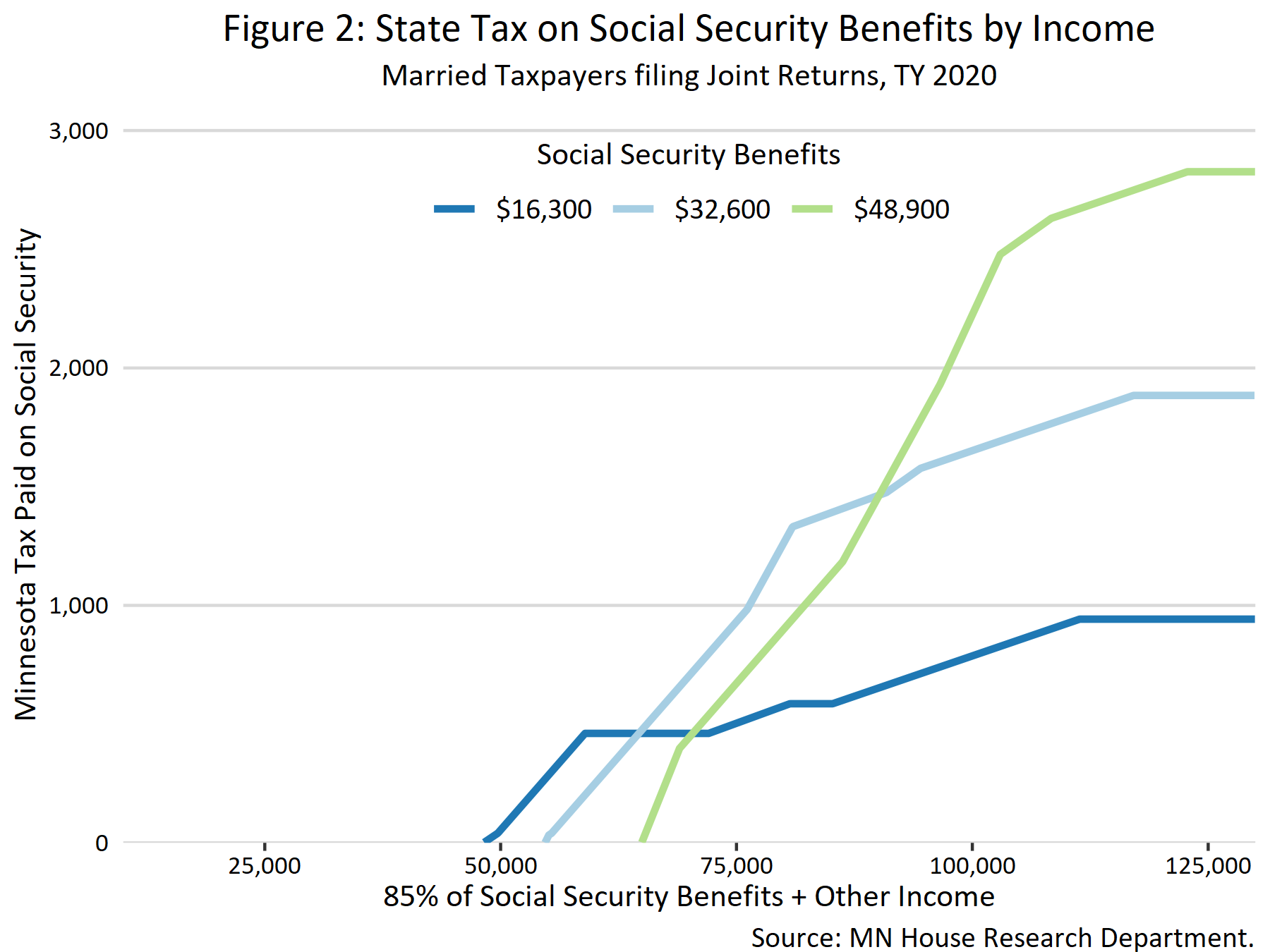

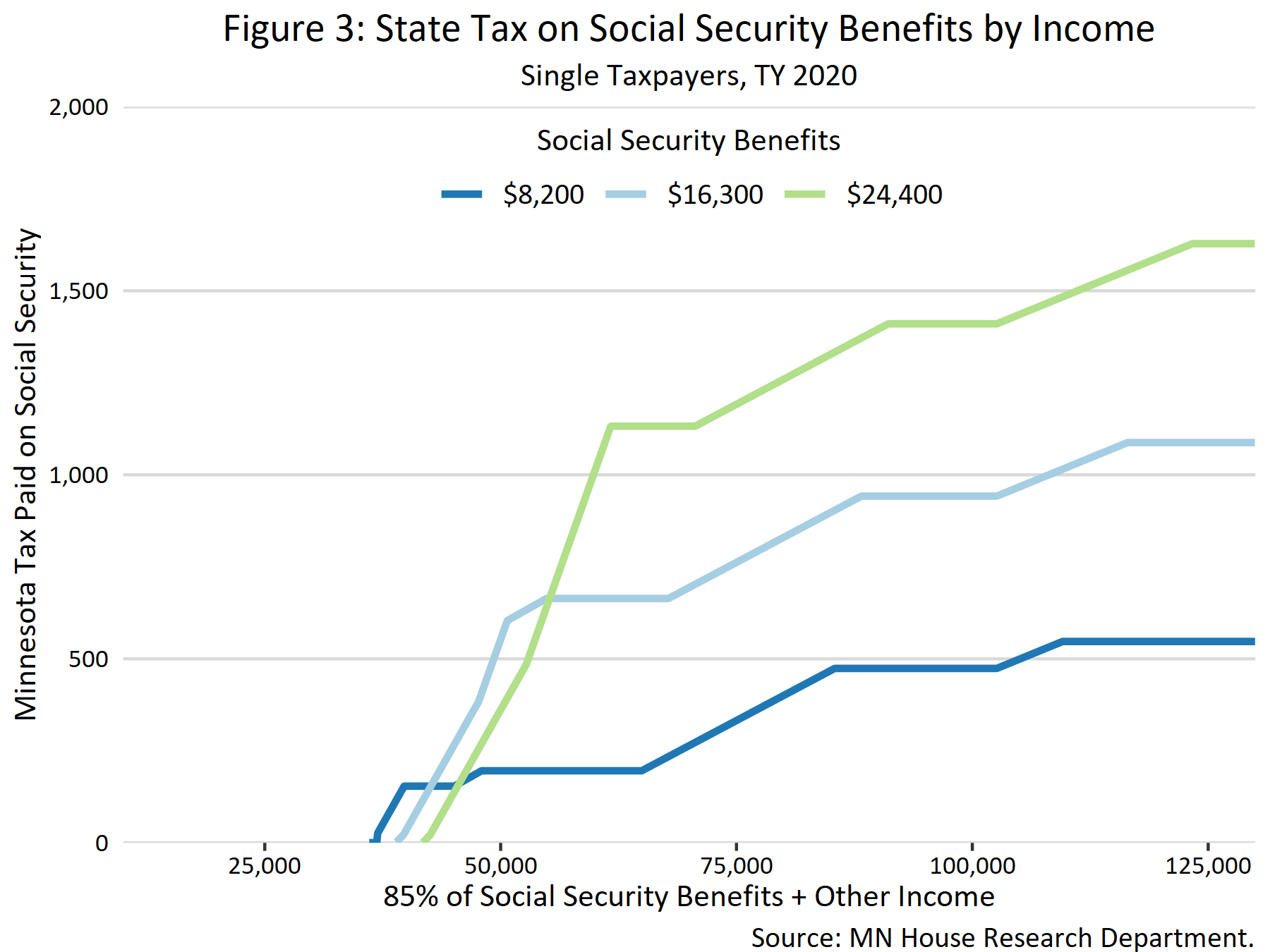

Figures 2 and 3 show the actual country tax paid on Social Security benefits, as a taxpayer'south total income increases. The graphs show the country tax on 3 different benefit amounts, depending on the taxpayer's total income. The benefit amounts called equal 50 percent, 100 percent, and 150 percent of the boilerplate Social Security benefit among Minnesota beneficiaries. For single taxpayers, the average benefit is for one beneficiary, and for married taxpayers, the boilerplate do good amount assumes each spouse is a beneficiary. The estimates are for tax year 2020, and assume taxpayers are 65 years or older and claim the standard deduction.11 The graphs also presume the taxpayer had no above-the-line deductions or nontaxable income.

Figures 2 and 3 deliberately use a measure of income that is very broad (85 percent of benefits plus "other income"), which captures a taxpayer'due south ability to pay taxes better than FAGI or conditional income. Two taxpayers with the same "income" level may pay different amounts of tax on their Social Security benefits. Counterintuitively, in some cases a taxpayer with a larger benefit corporeality will pay less tax on their benefits than another taxpayer with the aforementioned income level and a smaller benefit corporeality. This is considering the taxpayer with the larger benefit amount has a greater corporeality of their income excluded under the federal exclusion and land subtraction, resulting in less tax

The Reason for Taxing Social Security Benefits

Social Security benefits are partially taxed at the federal level, and the federal taxation treatment flows through to Minnesota's income tax. Minnesota'due south income tax uses federal adjusted gross income (FAGI) equally the starting indicate for its state revenue enhancement calculations. For taxpayers whose benefits are taxable federally, FAGI includes the taxable portion of their benefits, meaning Social Security is included in the income definition that is the starting point for Minnesota'south income taxation.

A widely accepted principle of tax policy is horizontal equity—that taxpayers with the aforementioned incomes should pay the same amount of tax, regardless of the source of the income. As a thing of taxation policy, the rationale for taxing Social Security benefits is that they are income and should be taxed like other sources of income. These horizontal equity concerns were part of Congress'south rationale for subjecting benefits to taxation in 1983. The Congressional Research Service (CRS) quotes the Business firm Ways and Means Commission equally arguing in 1983 that "social security benefits are in the nature of benefits received under other retirement systems, which are subject to taxation to the extent they exceed a worker'due south afterward-taxation contributions."12

CRS also raises a 2nd reason that benefits are taxed—to enhance revenue. The Social Security Amendments of 1983 devoted the revenue raised by taxing Social Security to improving the Social Security programme'southward solvency, and some states conformed to the federal treatment as a mode to raise acquirement.

Double Taxation of Benefits; Comparison with Other Forms of Retirement Savings

The revenue enhancement treatment of private alimony income and retirement savings accounts is designed to avoid double taxation. Retirement income is typically taxed either when the income is saved/contributed, or at the time the income is received, but not both. For example, traditional individual retirement accounts (IRAs) provide contributions are made pretax and retirement distributions are taxable, while contributions to Roth accounts are taxed in the yr made and qualifying distributions are not taxed. Traditional defined benefit pensions are taxable but retirees are allowed to recover a portion of their after-tax contributions tax free, each year under actuarial estimates of the corporeality contributed.

Congress designed the federal tax treatment of Social Security benefits to mimic the treatment of defined do good pensions—in other words, Congress intended for benefits to be taxed only to the extent that they exceed a percent of benefits received, determined actuarially to let recovery of employee taxes/contributions on average. Because the wages that pay Social Security taxes (FICA taxes) are subject field to income tax, they are analogous to post-tax employee contributions to a defined benefit pension plan.

In 1993, when the maximum share of Social Security benefits subject to taxation was increased to 85 percentage, the Social Security Actuary estimated that the average ratio of employee payroll revenue enhancement contributions to benefits received was about iv pct to 5 percent for current beneficiaries. For workers inbound the workforce in 1993, the Actuary estimated that the ratio was about 7 percent. The group with the highest estimated ratio of taxes paid to benefits received—unmarried, highly paid males—was about 15 percent. The federal exclusion for Social Security benefits was consequently set at xv percent to ensure that the taxpayers with the highest ratio of taxes paid to benefits received were non subject field to double revenue enhancement.13 The Social Security Actuary has not published updated estimates of the ratio of taxes paid to benefits received, so it is unclear if taxpayers with a high ratio of taxes paid to benefits received are currently subject to a pocket-sized amount of double taxation.

The Federal Social Security Exclusion

The starting point for calculating Minnesota's income tax is Federal Adjusted Gross Income (FAGI), which is a federally defined measure of income minus sure exclusions (also known as "above-the-line" deductions). Any income that is not included in FAGI is not subject field to Minnesota's income tax.

Federal law allows taxpayers to exclude a portion of their Social Security benefits when calculating FAGI, and this exclusion consequently flows through to Minnesota's income taxation. The formula used to calculate the exclusion is complicated; the amount of a taxpayer's exclusion depends on the taxpayer's provisional income (provisional income is discussed in particular below). Social Security benefits included in FAGI are bailiwick to federal tax in the same manner as ordinary income (e.m., wage, salary, and involvement income).

The federal Social Security exclusion has 3 tiers. Depending on the taxpayer'southward provisional income, the federal exclusion is either 100 percentage, l percentage, or fifteen percent of benefits. The table beneath shows the income ranges for the different tiers.

| Married Couple'southward Provisional Income | Single Filer'south Conditional Income | Exclusion Percentage |

|---|---|---|

| $32,000 or less | $25,000 or less | 100% |

| Tier 1: $32,000 to $44,000 | Tier 1: $25,000 to $34,000 | 50% |

| Tier 2: $44,000 or greater | Tier 2: $34,000 or greater | xv% |

Taxpayers with conditional income below the commencement tier threshold are allowed to exclude 100 percentage of their Social Security benefits. For taxpayers with provisional income betwixt the showtime and 2nd tier thresholds, the amount of benefits subject to federal tax equals the bottom of:

- l percentage of provisional income over the first tier threshold; or

- fifty percent of Social Security benefits.

For taxpayers with provisional income above the second tier threshold, the amount of benefits subject to federal tax equals the bottom of:

- 85 percent of provisional income over the 2d tier threshold, plus fifty percent of the difference between the second and first tier thresholds; or

- 85 percent of benefits.

Conditional Income

Conditional income is a federal definition of income equal to FAGI, excluding taxable Social Security benefits, plus certain "above-the-line" deductions, plus nontaxable interest, plus fifty percent of Social Security benefits. The deductions that are added dorsum in calculating provisional income are: adoption expenses, student loan involvement, tuition expenses, certain foreign income, and income from Puerto Rico and certain other U.South. territories. The formula for conditional income is equally follows:

Conditional Income

= FAGI-Taxable Social Security Benefits+50% of Social Security Benefits+Nontaxable Interest+Sure "above the line" deductions

History of Federal Handling

Social Security benefits were exempt from federal income taxes prior to 1983, when Congress subjected a portion of benefits to federal revenue enhancement. The Social Security Amendments of 1983 subjected up to l percent of a taxpayer'due south Social Security benefits to federal taxes, beginning in 1984. The amendments field of study merely Title 2 Social Security benefits and Tier 1 Railroad Retirement benefits to this treatment. Title 2 benefits are Old-age, Survivor's and Disability benefits—they practice not include Supplemental Security Income (SSI). The Omnibus Budget Reconciliation Act of 1993 added the second tier to the federal calculation, which subjected up to 85 percent of taxpayer's Social Security benefits to federal taxation.

Minnesota's Social Security Subtraction

Minnesota allows a subtraction for a portion of a taxpayer's Social Security benefits that are subject to federal tax. A taxpayer may claim the subtraction in improver to the federal exclusion. Taxpayers may subtract a portion of their benefits that are taxable federally, upward to a maximum established in law.

In tax yr 2017, the most recent year for which information is available, about 290,000 Minnesota taxpayers benefited from the subtraction, resulting in a revenue decrease of about $58.3 million. The average tax savings from the subtraction was nigh $201.

In tax year 2022 the maximum subtraction is $5,240 for married taxpayers filing articulation returns and $4,090 for unmarried taxpayers. The subtraction is phased out based on a taxpayer'due south provisional income—in tax yr 2020, the phaseout begins at $79,480 for married couples filing joint returns and $62,090 for unmarried taxpayers. The maximums and thresholds are adjusted annually for inflation.

Legislative History of the Minnesota Subtraction

2017 Legislature: Subtraction Established

The legislature established the Minnesota Social Security Subtraction in the 2022 omnibus tax bill.14 The original subtraction was for upwardly to $4,500 in federally taxable benefits for married couples filing joint returns and $3,500 for single taxpayers and heads of household. The maximum subtraction was phased out kickoff at $77,000 for married couples filing joint returns and $60,200 for unmarried taxpayers and heads of household. The legislature indexed both the maximum subtraction and phaseout thresholds for inflation.

2019 Legislature: Expansion of Maximums

The 2022 coach tax bill increased the maximum subtraction amounts, while slightly reducing the phaseout thresholds.15 The Section of Revenue estimated that the increase in the subtraction resulted in a revenue reduction of about $iv.4 million in taxation year 2019, and would grow to $5.iii million in FY 2023.

The pecker increased the maximum subtraction by $450 for married taxpayers filing joint returns and $360 for single taxpayers and heads of household. The legislature additionally reduced the phaseout thresholds by $2,250 for married couples filing joint returns and $1,800 for single taxpayers and heads of households. The reduction in the phaseout thresholds did non reduce any taxpayer'southward subtraction—it denied the do good of the increase in the maximum subtraction to taxpayers above the phaseout thresholds

Taxpayer Instance Lookup

The following tool estimates state income taxation liability for a taxpayer with social security income.

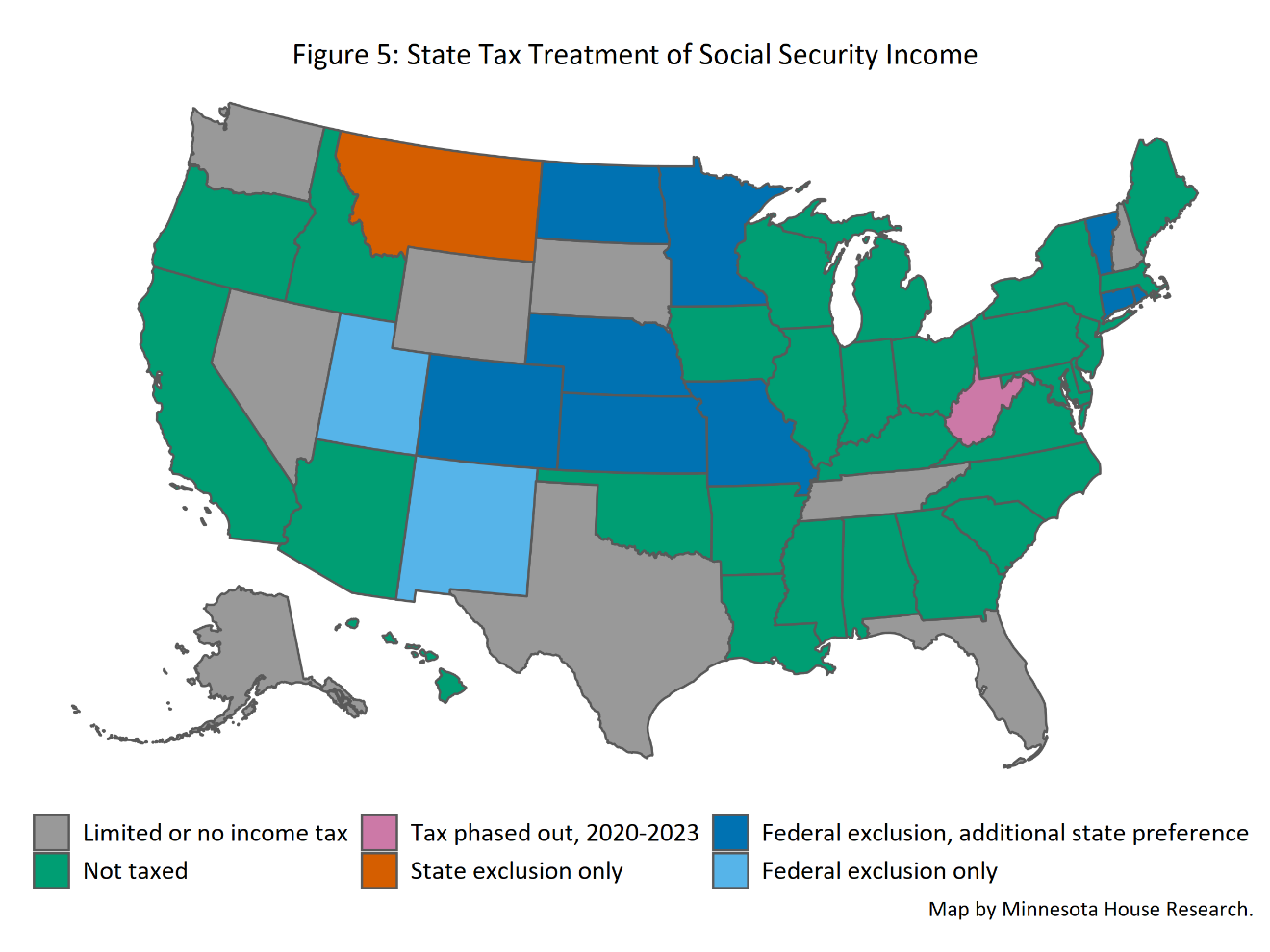

Tax Treatment of Social Security in Other States

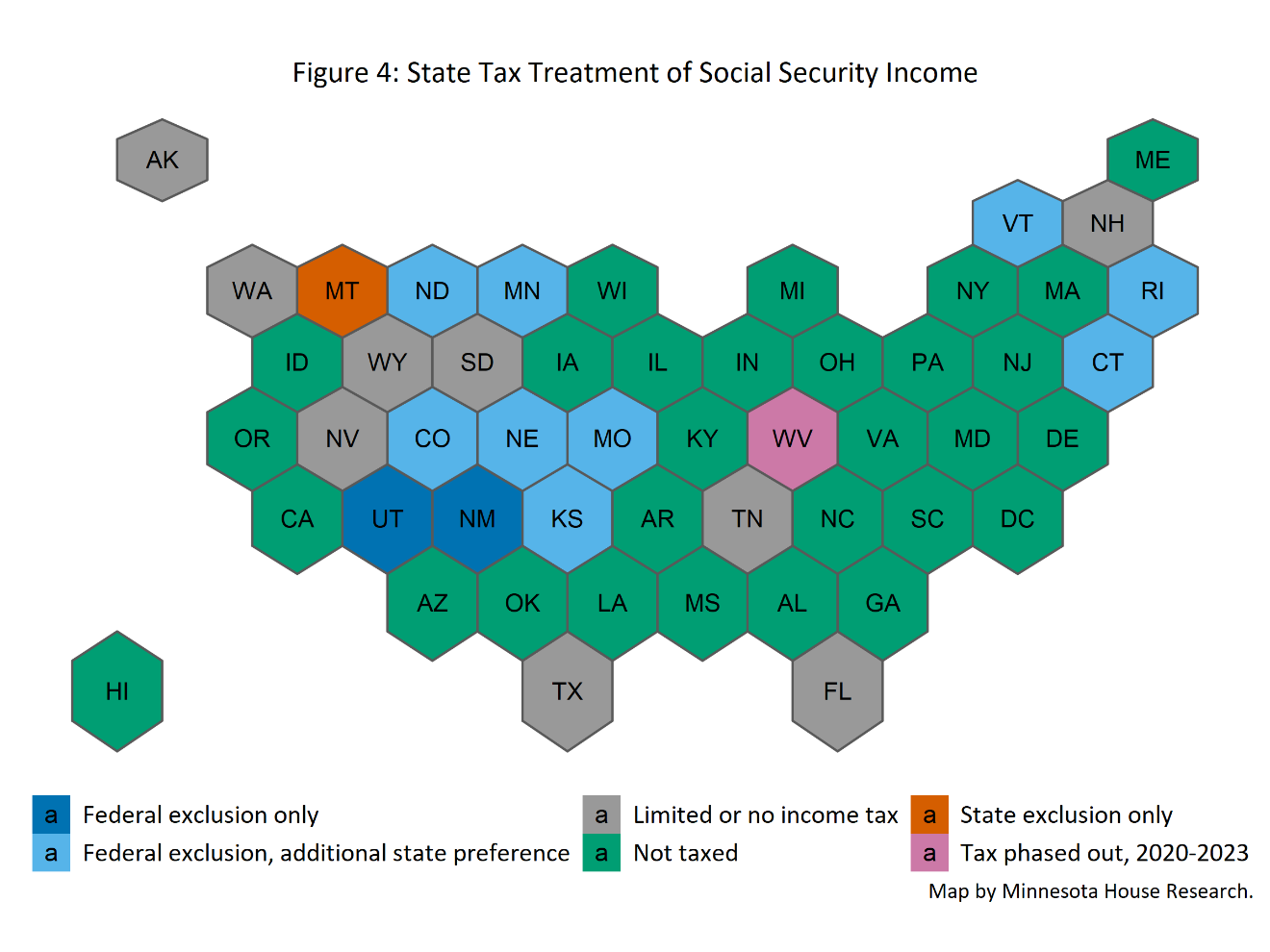

Figures 4 and 5 beneath bear witness the different tax treatments for Social Security benefits in the various states. Nine states exercise not have an income tax or have a tax express to specific kinds of unearned income. The states: Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming.

Xx-viii states with an income taxation, plus the District of Columbia, fully exempt Social Security benefits from the individual income tax. The states: Alabama, Arizona, Arkansas, California, Delaware, District of Columbia, Georgia, Hawaii, Idaho, Illinois, Indiana, Iowa, Kentucky, Louisiana, Maine, Maryland, Massachusetts, Michigan, Mississippi, New Bailiwick of jersey, New York, Northward Carolina, Ohio, Oklahoma, Oregon, Pennsylvania, South Carolina, Virginia, and Wisconsin.

Fourteen states subject area at least a portion of Social Security to country taxes, ane of which is scheduled to allow a full exemption in 2022. Most states in this grouping (Colorado, Connecticut, Kansas, Minnesota, Missouri, Nebraska, North Dakota, Rhode Island, and Vermont) allow the federal exclusion, but offering boosted deductions or exemptions for taxpayers of certain ages or beneath certain income levels. Table 5 describes these preferences in item.

| State | Type of Benefit | Description |

|---|---|---|

| Colorado | Retirement income preference | Taxpayers ages 65 and older may subtract upwardly to $24,000 of taxable pension and annuity income (including Social Security). |

| Connecticut | Income-tested exemption | Exempt for married taxpayers with less than $100,000 of AGI and singles with $75,000 of AGI. Subtraction is phased out above those thresholds. |

| Kansas | Income-tested exemption | Exempt for taxpayers with less than $75,000 or less of AGI. |

| Minnesota | Income-tested exemption | Subtraction for upwardly to $five,240 of federally taxable benefits for married couples filing jointly ($4,090 for single taxpayers). Phased out at $79,480 of provisional income for married taxpayers and $62,090 for other taxpayers. (Tax yr 2020; thresholds are adapted for inflation). |

| Missouri | Income-tested exemption | Exempt for married taxpayers with less than $100,000 of AGI and singles with $85,000 of AGI. Subtraction is phased out above those thresholds. |

| Montana | State-specific exemption | Does not recognize the federal exemption, and instead calculates a state-specific exemption corporeality. |

| Nebraska | Income-tested exemption | Exempt for married taxpayers with less than $58,000 of AGI and singles with $43,000 of AGI. |

| New United mexican states | Exemption for senior taxpayers | Taxes the same amount of benefits that are taxable federally, but provides an additional exemption amount for all taxpayers 65 or older. |

| North Dakota | Income-tested exemption | Exempt for married taxpayers with less than $100,000 of AGI and singles with $50,000 of AGI. |

| Rhode Island | Income-tested exemption | Exempt for married taxpayers 65 or older with $106,400 of AGI and singles with $85,150 of AGI. (Tax year 2019; thresholds are adjusted for aggrandizement.) |

| Utah | Retirement credit | Taxes the same amount of benefits as are taxable federally, but allows a retirement credit of upwardly to $450 per taxpayer 65 years or older. Some taxpayers under 65 with retirement income are as well eligible. Phased out at $35,000 for married joint filers and $25,000 for singles. |

| Vermont | Income-tested exemption | Exempt for married taxpayers with less than $threescore,000 of AGI and singles with $45,000 of AGI. Exemption is phased out in a higher place those thresholds. |

| West Virginia | Phasing out tax on benefits | 35% exclusion for federally taxable benefits for revenue enhancement year 2020. The exclusion will increment to 65% in revenue enhancement year 2021, and 100% in tax twelvemonth 2022. |

History of Social Security Tax in Minnesota

Minnesota historically conformed to the federal tax treatment of Social Security income. For revenue enhancement years 1983 and prior, Social Security benefits were exempt from tax at the federal and state level. Showtime in tax yr 1984, Congress subjected Social Security benefits to federal tax. Minnesota initially did not conform to the federal handling, and for tax year 1984, the state allowed a subtraction for Social Security benefits that were taxable federally. In 1985, the land repealed the subtraction, and followed the federal treatment until tax year 2017. The 2022 legislature established a land subtraction for a portion of taxable benefits, effective in tax year 2017.

| Tax Yr | Federal Tax Treatment | Minnesota Taxation Treatment |

|---|---|---|

| 1983 and prior | Fully exempt | Fully exempt |

| 1984 | Upwardly to 50% of benefits taxed | Fully exempt |

| 1985-1993 | Up to 50% of benefits taxed | Upward to l% of benefits taxed |

| 1994-2016 | Upwardly to 85% of benefits taxed | Up to 85% of benefits taxed |

| 2017 and afterwards | Upwards to 85% of benefits taxed | Up to 85% of benefits taxed, less state subtraction for amounts taxable federally |

Footnotes

1 Render data estimated using the House Income Tax Simulation model (HITS) version 6.9.

2 House Research judge. Assumes 74 percent of households that received Social Security benefits filed a Minnesota return.

four The Social Security Administration reported that 1,012,620 beneficiaries received Social Security benefits in Minnesota equally of December 2017. Because many of those individuals filed articulation income tax returns, the estimate of 784,000 returns is plausible. Social Security Assistants Annual Statistical Supplement, 2018; https://www.ssa.gov/policy/docs/statcomps/supplement/2018/supplement18.pdf.

5 This is like to a projection from the Minnesota Section of Acquirement Tax Research Sectionalisation, which estimates that 43 percent of households that included a Social Security beneficiary volition pay revenue enhancement on their benefits in tax year 2021. The Tax Research Division projects that most 767,000 households in Minnesota volition receive Social Security benefits in revenue enhancement year 2021. Minnesota Section of Acquirement Tax Research Partition, Taxability of Social Security Income: Tax Yr 2021, projections from the 2022 Minnesota Tax Incidence Summary, April 25, 2019.

six Laws 2019, 1st spec. sess. ch. 6, fine art. 2, sec. 12. A preliminary assay showed that the 2022 expansion reduced this gauge of the share of benefits subject field to revenue enhancement by less than 1 percentage point.

viii Provisional income is described in item in a afterwards section.

10 Taxpayers with big business losses could theoretically have provisional income that is less than half of their benefits.

xi Taxpayers ages 65 and older receive a slightly larger standard deduction.

12 Paul Davies, Congressional Research Service, Social Security: Taxation of Benefits, November 1, 2019.

thirteen Ibid, pages 15-16.

August 2020

Source: https://www.house.leg.state.mn.us/hrd/issinfo/sstaxes.aspx

0 Response to "House of Representatives Office of Payroll and Benefits"

Postar um comentário